In this glided age of technology, with the rapid expansion of software development and internet access worldwide the future of banking is becoming more and more digitalized. Do you want to open a bank account, transfer money, or exchange money without risks? You can do it all online without standing in long lines, wasting time, and spending extra money on gas. The truth is that digitalized banking processes have changed our lives. In this blog article, we will discuss what neobanks are, how they are shaping the future of banking, and if they can replace the traditional ones.

What are neobanks?

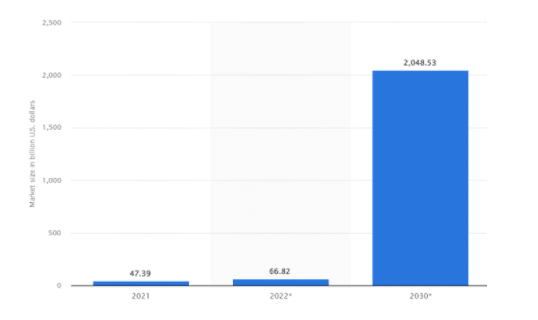

Neobanks, or so called the future of banking,provide software solutions and other technologies to streamline mobile, online banking, and fintech products. Typically, neobanks specialize in particular financial products. They are considered more transparent and agile than traditional banking services, even though many have partnerships with conventional banks to insure their financial products. According to a Statistareport, the global neo-banking market was valued at $47.39 billion in 2021. It is estimated to grow at an annual average rate (CAGR) of 53.4 percent by 2030, reaching a value of $2.05 trillion U.S dollars that year. More and more businesses will require fintech solutions to optimize their payments and transactions in order to overall improving their customer experience.

Source:Statista, 2022. The market size of neobanks in 2021 with a forecast for 2022 and 2030.

Why are neobanks the future of banking?

Contrary to traditional banks with complex technology protocols, neobanks have complex and powerful databases that are easy to exploit from the outset. The advantages of switching to neobanking services include lower fees for banking services, smoother UI, and more autonomy. They do not follow traditional legal bank policies and requirements and are easier to use – you may make your bank account in less than 5 minutes.

So, are neobanks the future of banking?

According to previous arguments yes, they are!

Neobanking pros

– Speed – you don’t need to wait several days for a credit card; it is released instantly

– Cost saving – online banks have lower operating costs. Neobanking offers higher interest rates for saving accounts, one of its most significant advantages. Some players on the market may offer interest rates from 0.5% to 2.5%. Traditional banks usually provide 0.0% to 0.2% interest rates, as stated in the report on deposit rates worldwide done by The World Bank.

– Simple to use – neobanking apps offer a rich customer experience, from the personalization of the experience in the app to a simple interface that 10-year-olds can easily understand.

Neobanking cons

– No physical location – as neobanks operate online, you cannot get a loan, experience face-to-face interaction with bank workers and accounts, or take out a loan.

– Withdrawing money for a fee – if you prefer to keep banknotes over having your money stored in a bank account, neobanks might not be the right choice. Many neobanks perceive a fee for withdrawing money from ATMs, meaning that your virtual card should be your best friend instead of traditional money.

Can neobanks replace traditional banks shortly?

With a completely digital offering, neobanks, appear to be the future of banking combined with solutions created by custom enterprise software development specialists. They appeal to both young people and small and medium enterprises, which are major growth sectors. Nevertheless, they will likely be market leaders in the next few years due to their modern technological systems, low or no-cost accounts, higher saving rates, and customized financial solutions.

// If you’re looking for a software services partner to help your business adapt to change, leave us a message